On This Page

1. What is Medicare Plan F?

Medicare Plan F, also called Medicare Supplement Plan F, is a comprehensive Medigap policy designed for people enrolled in Original Medicare (Part A and Part B).

It helps cover almost all out‑of‑pocket costs that Original Medicare doesn’t pay, including Medicare Part A and Part B deductibles, coinsurance, copayments, skilled nursing facility coinsurance, excess charges, and certain emergency medical costs when traveling outside the U.S.

Because it fills nearly every gap in Original Medicare, Plan F offers predictability and peace of mind for beneficiaries who expect frequent medical care or want to avoid unexpected expenses.

However, Plan F is only available to people who were first eligible for Medicare before January 1, 2020; those who became eligible after that date can no longer buy this plan.

The overview of Medicare Plan F. (Image by Unsplash)

2. What is Medicare Plan G?

Medicare Plan G, also known as Medicare Supplement Plan G, is a Medigap policy designed for people enrolled in Original Medicare (Part A and Part B).

It helps cover most out-of-pocket costs that Medicare doesn’t pay, such as Part A and Part B coinsurance, skilled nursing facility coinsurance, hospice care, the first three pints of blood, excess charges, and certain foreign travel emergency costs.

The main difference from Plan F is that Plan G does not cover the Part B deductible. Plan G is ideal for beneficiaries who want strong financial protection against unexpected medical expenses, especially those newly eligible for Medicare after January 1, 2020, who can no longer purchase Plan F.

3. Medicare Plan F vs Plan G: Full Side-by-Side Comparison

Choosing between Medicare supplement Plan F vs G can feel tricky, but understanding the differences helps you pick the right coverage for your healthcare needs.

Both plans are Medigap options that fill the gaps left by Original Medicare, yet they differ in cost, availability, and what you pay out-of-pocket, making a side-by-side look essential for comparison.

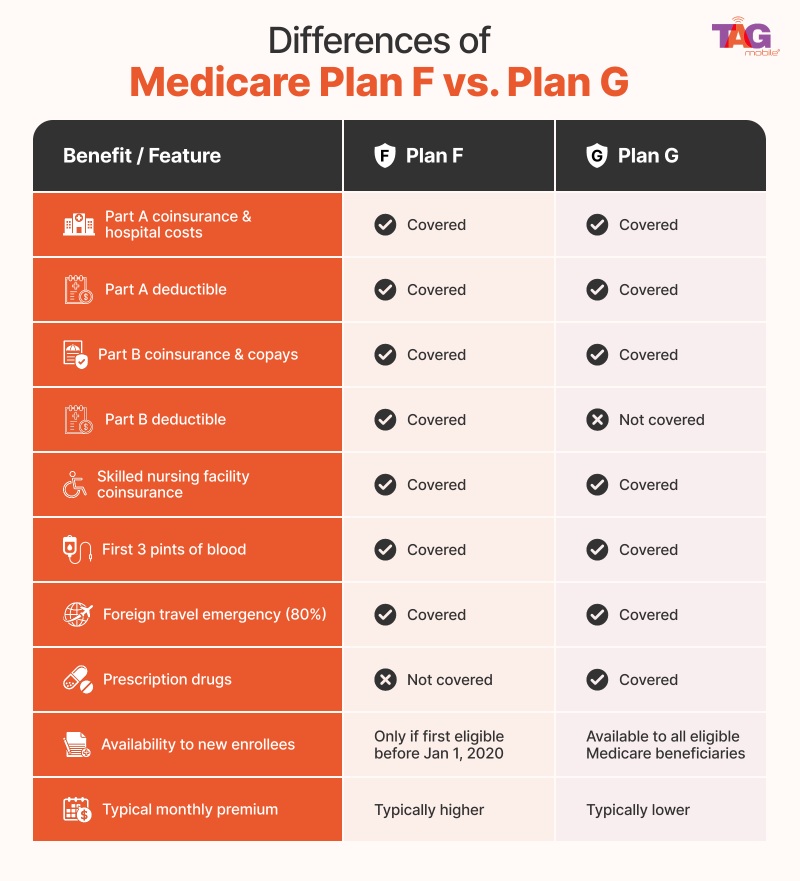

| Benefit / Feature | Plan F | Plan G |

|---|---|---|

| Part A coinsurance & hospital costs | Covered | Covered |

| Part A deductible | Covered | Covered |

| Part B coinsurance & copays | Covered | Covered |

| Part B deductible | Covered | Not covered |

| Skilled nursing facility coinsurance | Covered | Covered |

| First 3 pints of blood | Covered | Covered |

| Foreign travel emergency (80%) | Covered | Covered |

| Prescription drugs | Not covered | Not covered |

| Availability to new enrollees | Only if first eligible before Jan 1, 2020 | Available to all eligible Medicare beneficiaries |

| Typical monthly premium | Typically higher | Typically lower |

4. Medicare vs Medicaid: Don’t Confuse These Programs

Medicare and Medicaid are both government-run programs that help people access healthcare, but they serve different populations and have different eligibility rules.

Medicare primarily provides health coverage for people aged 65 and older, as well as certain younger individuals with disabilities or specific conditions. It helps cover hospital stays, medical services, and sometimes prescription drugs, but most enrollees still have some out-of-pocket costs and may choose supplemental insurance to fill the gaps.

On the other hand, Medicaid is a needs-based program that provides health coverage for low-income individuals and families, including children, pregnant women, and people with disabilities.

One of the biggest differences is that Medicaid recipients may qualify for the Lifeline program and receive other benefits beyond healthcare, such as discounted phone and internet services, food assistance, and transportation support.

Some people mistakenly believe they can get a “free phone with Medicare.”

In reality, Medicaid (not Medicare) is one of the qualifying programs for Lifeline.

5. How Lifeline Helps Reduce Monthly Expenses with Medicaid?

Medicaid is one of the assistance programs that can qualify recipients for the Lifeline program, helping to reduce monthly expenses by providing access to discounted or free phone and internet services.

These benefits make it easier for low-income households to stay connected and save money that can be spent on essential needs. While evaluating healthcare costs, such as Medicare Plan F vs Plan G cost, enrolling in Lifeline can offer additional financial relief beyond medical coverage.

- Check your eligibility by confirming you are enrolled in Medicaid or meet income requirements

- Prepare documents such as your Medicaid approval letter, benefits card, and a valid form of identification

- Choose a plan and select a free smartphone or SIM/eSIM option that fits your needs

- Complete the application by providing accurate personal information and uploading required documents if needed

- Submit your application and wait for approval from the provider

- Once approved, receive your device (typically within 7-10 business days) and follow the included activation instructions

6. Final Words

Choosing the right Medicare plan F vs plan G pros and cons can make a big difference in managing your healthcare expenses. While Plan F offers the most complete coverage for those already eligible, Plan G provides nearly the same benefits at a lower cost and is available to most new Medicare enrollees. Understanding the differences, including out-of-pocket costs and coverage details, helps you make an informed decision that fits your needs.